CN 1 October 1, 2006

CANCELLATION/NULLIFICATION

Flood insurance coverage may be terminated at

any time, by either canceling or nullifying the policy

depending upon the reason for the transaction. If

coverage is terminated, the insured may be entitled

to a full or partial refund under applicable rules and

regulations. In some instances, the insured might

be ineligible for a refund.

I. PROCEDURES AND VALID REASONS

Submit a completed Cancellation/Nullification

Request Form and proper documentation to the

current NFIP insurer for processing.

A. Refund Processing Procedures

1. The current NFIP insurer (WYO Company

or Direct Business) will be responsible for

returning the premium for the current and 1

prior policy year, provided that it was the

insurer for that period. If another NFIP

insurer was the insurer for the prior policy

year, it will be responsible for returning the

premium for that year.

2. Requests for refunds for more than 2 years

(Reason Codes 4, 6, 10, 16, and 22 only)

must be processed by the NFIP Bureau.

a. For requests processed by the Bureau,

the current NFIP insurer must submit all

of the documentation necessary to

make a refund for any period exceeding

2 years. At a minimum, this docu-

mentation will consist of the following:

• A policy cancellation request and

the premium refund calculation for

each year.

• The company’s statistical records or

declarations pages for each policy

term and evidence of premium pay-

ments obtained from the insured if

these documents are not available

from the company’s records.

• Photographs to verify ineligible risks.

• For Cancellation Reason Code 22

only (standard policy eligible for PRP):

A Letter of Map Amendment (LOMA);

a Letter of Map Revision (LOMR); a

copy of the most recent flood map

marked to show the exact location

and flood zone of the building; a letter

indicating the exact location and flood

zone of the building, and signed and

dated by a local community official; an

Elevation Certificate indicating the

exact location and flood zone of the

building, and signed and dated by a

surveyor, engineer, architect, or local

community official; or a flood zone

determination certification that guar-

antees the accuracy of the

information.

b. Mail the appropriate documentation to the

NFIP Bureau and Statistical Agent,

Under-writing Department, P.O. Box 310,

Lanham, MD 20703.

3. WYO Companies will be notified of the

premium refunded and the Expense

Allowance due to the NFIP. The companies

must maintain this documentation as part of

their underwriting files.

4. The insured must have a current NFIP policy

to be eligible for a refund of any prior year’s

premium. All existing refund rules concerning

the Federal Policy Fee and producer

commission remain in effect.

TRRP reason codes in this section are used for

reporting purposes only.

B. Reason Codes for Cancellation/

Nullification of NFIP Policies

1. Building Sold or Removed. (TRRP

reason 01)

The insured has sold or transferred

ownership of the insured property and no

longer has an insurable interest; the builder

or developer has requested to cancel the

policy mid-term because a newly created

association has purchased a policy under

its name; or the insured property has been

removed from the described location. This

reason code also may be used if the

building has been foreclosed or if the

building is considered a total loss because

the building damage is greater than or

equal to the replacement cost of the

building. The effective date of the

cancellation is the date the insured ceased

to have an insurable interest in the

property. For buildings sold, proof-of-sale

documentation is required.

y Type of Refund: Pro Rata

y Years Eligible for Refund: Up to 2 years

y Cancellation Request: Must be received

within 1 year of date of sale or removal

y Documentation: Bill of sale, settlement

statement, foreclosure notice, proof of

removal, or proof of total loss

NEXT SECTION

TABLE OF CONTENTS

PREVIOUS SECTION

CN 2 May 1, 2005

2. Contents Sold or Removed. (TRRP

reason 02)

The insured has sold or transferred

ownership of the insured property and no

longer has an insurable interest, or the

insured property has been completely

removed from the described location. The

effective date of the cancellation is the date

the insured ceased to have an insurable

interest in the property at the described

location, or the date the property was

removed from the described location.

y Type of Refund: Pro Rata

y Years Eligible for Refund: Up to 2 years

y Cancellation Request: Must be received

within 1 year of date of sale or removal

y Documentation: Bill of sale, proof of

contents removal, or proof of total loss

3. Policy Canceled and Rewritten To

Establish a Common Expiration Date

with Other Insurance Coverage. (TRRP

reason 03)

The new policy must be rewritten within the

same company for the same or higher

amounts of coverage. However, if it is

rewritten for higher amounts of coverage,

the waiting period rule will apply. The

producer must submit a new Application

and premium. Upon receipt of the new

policy declarations page, the producer

should request cancellation of the prior

policy. The effective date of the cancellation

will be the same as the effective date of the

new policy.

y Type of Refund: Pro Rata

y Years Eligible for Refund: Current year

y Cancellation Request: Must be received

within 1 year of the new policy effective

date

y Documentation: Copy of new policy

declarations page

4. Duplicate NFIP Policies. (TRRP reason

04)

When a duplicate NFIP policy has been

issued, only one policy can remain in effect.

The insured can choose which policy is to

remain in effect and which policy is to be

canceled. This does not apply when there

has been a deliberate creation of duplicate

policies. If this event does occur, the policy

with the later effective date must be

canceled. Losses occurring under such

circumstances will be adjusted according to

the terms and conditions of the first policy.

When coverage has been force-placed by

a lender using a conventionally written

standard policy because the required

underwriting information is available, that

policy is considered equivalent to the

MPPP policy. The WYO Company is

authorized to cancel the standard (force-

placed) or the MPPP policy, provided that

a copy of the force-placement letter from

the mortgagee and a copy of the policy

declarations page are submitted with the

Cancellation/Nullification Request Form.

y Type of Refund: Pro Rata

y Years Eligible for Refund: Up to 6 years

y Cancellation Request: Must be received

within 1 year of the policy expiration

date

y Documentation: Copy of declaration

page(s) and, for the MPPP, a copy of

the force-placement letter from the

mortgagee

5. Non-Payment. (TRRP reason 05)

When a producer accepts a premium

payment from a client and then submits an

agency check to the NFIP with the

application, the policy may be nullified if the

client's check is returned because of

insufficient funds or any other reason the

check is not made good to the producer.

The bank's notice must be attached to the

form when this situation occurs. If the

producer can document this, a full premium

refund is provided to the producer. If a

WYO company has covered the premium

for a prospective insured and then does not

receive payment, the policy can be nullified.

This reason cannot be used if the producer

advanced agency funds and the client

simply refused to pay the agency.

y Type of Refund: Full

CN 3 May 1, 2005

y Years Eligible for Refund: Current year

y Cancellation Request: Must be received

during the policy year

y Documentation: Bank notice of non-

payment

6. Risk Not Eligible for Coverage. (TRRP

reason 06)

This reason is used to nullify a policy when

an application was submitted and a policy

issued on a property not eligible for

coverage. A clear and precise explanation

must be included when submitting this type

of cancellation request. Examples include:

- Property not located in a community

participating in the NFIP. (The use of an

incorrect community number allowed the

policy to be issued.)

- Contents located in an open building.

- Property is located in a Coastal Barrier

Resources System (CBRS) area.

y Type of Refund: Full

y Years Eligible for Refund: No limit, back

to policy inception

y Cancellation Request: Must be received

within 1 year of the policy expiration date

y Documentation: Tax records, Section

1316 declaration, or CBRA determi-

nation, as appropriate, or photographs

showing ineligibility

7. Property Closing Did Not Occur. (TRRP

reason 08)

This reason is used to nullify a policy when

a policy is issued for a closing at the time of

settlement on a property and the transfer of

the property does not take place. The client

does not actually acquire an insurable

interest in the property.

y Type of Refund: Full

y Years Eligible for Refund: Current year

y Cancellation Request: Must be received

during the policy year

y Documentation: Statement from title

company, lender, or attorney

representing the interests of title

company, lender, or insured, that the

property closing did not occur

8. Policy Not Required by Mortgagee.

(TRRP reason 50)

This provides a means to cancel a policy

when coverage was required by the

mortgagee for a closing and it was later

determined that the property was not

located in a Special Flood Hazard Area

(SFHA). As a result, coverage was not

required by the mortgagee. The

mortgagee’s statement to this effect must

be attached to the Cancellation/Nullification

Request Form.

This cancellation reason can be used only if

the cancellation request was made during

the initial policy term. The cancellation

effective date is the date the cancellation

request is received by the writing company.

A revised determination from the lender

may be used to cancel the policy. A FEMA

Out-As-Shown Determination, as a result of

a LOMA application, is needed if there is a

discrepancy between the lender’s and the

insured’s determinations.

NOTE: This cancellation reason may be

used even if the policy was written as being

in a non-SFHA.

y Type of Refund: Pro Rata

y Years Eligible for Refund: Current year

y Cancellation Request: Must be received

during the policy year

y Documentation: Copy of original

mandatory purchase document and

current mortgagee statement that policy

is not required; a revised determination

from the lender showing that the

building is not in an SFHA.

9. Insurance No Longer Required by

Mortgagee Because Property Is No

Longer Located in a Special Flood

Hazard Area Because of a Physical Map

Revision. (TRRP reason 09)

Flood insurance was initially required by the

mortgagee or other lender because the

property was determined to be in an SFHA.

Following the physical revision of a map, if

the property is no longer located in an

SFHA, then the policy may be canceled

CN 4 October 1, 2005

provided the mortgagee confirms in writing

that the insurance is no longer required

because the property was removed from

the SFHA.

NOTE: RCBAP policies require a release

from the mortgagee of every unit owner in

the association or a statement of the unit

owner, if no mortgagee. Only after this

requirement is met can the policy be

canceled. The condominium association

must provide a signed letter that lists the

number of units and specifies the owner of

each unit.

y Type of Refund: Full

y Years Eligible for Refund: Current year

and for an additional policy year in

those cases where the insured had

been required to renew the policy

during the 6-month period when a

revised map was being reprinted,

provided no claim has been paid or is

pending during the policy year that is

being canceled

y Cancellation Request: Must be received

during the policy year or within 6

months of the policy expiration date

y Documentation: Statement from mort-

gagee that insurance was required as

part of mortgage but is no longer

required, and a copy of the revised map

10. Condominium Policy (Unit or

Association) Converting to RCBAP.

(TRRP reason 45)

This provides a means to cancel a

condominium policy because coverage is

being provided under an RCBAP. Duplicate

coverage occurs when the unit owner policy

and the RCBAP limits are more than the

cost of the unit, up to the maximum limits of

the Program.

y Type of Refund: A pro rata premium

refund, including Federal Policy Fee

and Probation Surcharge, is provided.

y Years Eligible for Refund: Up to 6 years

y Cancellation Request: Must be received

within 1 year of the policy expiration

date

y Documentation: Copy of RCBAP and

value of unit

12. Mortgage Paid Off. (TRRP reason 52)

This reason is used to cancel a policy that

was obtained due to a requirement by a

mortgagee or lender as a condition of a

mortgage loan, and that mortgage loan has

now been paid off.

y Type of Refund: Pro Rata

y Years Eligible for Refund: Current year

y Cancellation Request: Must be received

within 6 months of the date the

mortgage was paid off for the

cancellation to be effective on the date

of payoff. When the request is received

after 6 months, the effective date for

cancellation is the receipt date of the

request.

y Documentation: Statement from mort-

gagee that mortgage has been paid off

and that flood insurance was required

as part of mortgage

13. Voidance Prior to Effective Date. (TRRP

reason 60)

This reason is used when coverage is not

mandatory and a policyholder decides

during the 30-day waiting period, or prior to

the effective date of a renewal, not to take

the policy, after submitting a premium

payment.

y Type of Refund: Full

y Years Eligible for Refund: Current year

y Cancellation Request: Must be received

prior to the policy effective date

y Documentation: Policyholder’s request

14. Voidance Due to Credit Card Error.

(TRRP reason 70)

This reason is used when an error or billing

dispute occurs (processing error or fraud)

on a credit card payment.

y Type of Refund: Full

y Years Eligible for Refund: Current year

y Cancellation Request: Must be received

during the policy year

y Documentation: Credit card notice of

non-payment

CN 5 October 1, 2005

15. Insurance No Longer Required Based on

FEMA Review of Lender's Special Flood

Hazard Area Determination. (TRRP

reason 16)

Flood insurance was initially required by the

mortgagee or other lender because the

property was determined to be in a Special

Flood Hazard Area (SFHA). Following a

review under the Flood Disaster Protection

Act of 1973, as amended, FEMA issued a

Letter of Determination Review (LODR)

because the building or manufactured

home is not in an SFHA and insurance is

not required. The policy may be canceled

back to inception.

This cancellation reason can be used only if

the request from the borrower and lender

was sent to FEMA for a LODR within 45

days from the lender’s notification to the

borrower that the building is in an SFHA

and that flood insurance is required.

y Type of Refund: Full

y Years Eligible for Refund: Current year

provided no claim has been paid or is

pending

y Cancellation Request: Must be received

during the policy year or within 6

months of the policy expiration date

y Documentation: Copy of FEMA’s Letter

of Determination Review, and

statement from the lender that flood

insurance is not required

16. Duplicate Policies from Sources Other

Than the NFIP. (TRRP reason 17)

This reason code is used to cancel an NFIP

policy when a duplicate policy has been

obtained from sources other than the NFIP.

y Type of Refund: Pro Rata

y Years Eligible for Refund: Current year

y Cancellation Request: Must be received

within 6 months of the new policy

effective date. When the request is

received after 6 months, the effective

date for cancellation is the receipt date

of the request.

y Documentation: Copy of declarations

page of the new policy and a statement

from the mortgagee, if any, accepting

the non-NFIP policy as the replacement

18. Mortgage Paid Off on a Mortgage

Portfolio Protection Program (MPPP)

Policy. (TRRP reason 52)

This reason code is used to cancel an

MPPP Policy after the mortgage is paid off.

y Type of Refund: Pro Rata

y Years eligible for refund: Current year

• Cancellation Request: Must be received

within 6 months of the date the

mortgage was paid off for the

cancellation to be effective on the date

of payoff. When the request is received

after 6 months, the effective date for

cancellation is the receipt date of the

request.

y Documentation: Statement from mort-

gagee that mortgage has been paid off

and that flood insurance was required

as part of mortgage

19. Insurance No Longer Required by the

Mortgagee Because the Structure Has

Been Removed from the Special Flood

Hazard Area (SFHA) by Means of Letter

of Map Amendment (LOMA) or Letter of

Map Revision (LOMR). (TRRP reason 20)

Where flood insurance was required by the

mortgagee or other lender because the

property was determined to be in an SFHA,

and it is later determined that the property is

no longer located in an SFHA through the

issuance of a LOMA or LOMR, the policy

can be canceled provided the lender

confirms in writing that the insurance is no

longer required because the property was

removed from the SFHA. A copy of the

LOMA or LOMR must accompany this

request.

NOTE: RCBAP policies require a release

from the mortgagee of every unit owner in

the association or a statement of the unit

owner, if no mortgagee. Only after this

requirement is met can the policy be

canceled. The condominium association

must provide a signed letter that lists the

number of units and specifies the owner of

each unit.

• Type of Refund: Full

CN 6 October 1, 2005

• Years Eligible for Refund: Current year

and, if applicable, 1 prior year provided

no claim has been paid or is pending

during the policy year that is being

canceled

• Cancellation Request: Must be received

during the policy year or within 6 months

of the policy expiration date

y Documentation: Statement from mort-

gagee that flood insurance is no longer

required because the property was

removed from the SFHA, and a copy of

the LOMA/LOMR

20. Policy Was Written to the Wrong Facility

(Repetitive Loss Target Group). (TRRP

reason 21)

This reason is used to cancel a policy flat

when coverage was inadvertently written to

the wrong facility on those structures that

were identified as part of the Repetitive

Loss Target Group. The cancellation

effective date must be the same as the

policy effective date.

y Type of Refund: Full

y Years Eligible for Refund: Current year

y Cancellation Request: Must be received

during the policy year

y Documentation: Repetitive Loss Target

Group Report provided by the NFIP

Bureau and Statistical Agent

21. Other: Continuous Lake Flooding or

Closed Basin Lakes. (TRRP reason 10)

This cancellation code is used for

continuous lake flooding or closed basin

lakes. The cancellation can be for only one

term of a policy. The cancellation effective

date must be after the date of loss.

y Type of Refund: No refund allowed

y Years Eligible for Refund: N/A

y Cancellation Request: N/A

y Documentation: FEMA notification

22. Cancel/Rewrite Due to Misrating. (TRRP

reason 22)

This reason code is used when ineligible

PRPs or MPPP policies are canceled and

rewritten and when changes are made due

to system constraints. The code should also

be used to cancel a standard policy that is

eligible for a PRP. Refunds resulting from

the cancellation must be applied to the

rewritten policy prior to any refund being

generated. Use rollover indicator “Z” to

report the new policy.

y Type of Refund: Full

y Years Eligible for Refund: Up to 6 years

y Cancellation Request: N/A

y Documentation: LOMA, LOMR, zone

determination, copy of map, etc.

23. Fraud. (TRRP reason 23)

This reason code is used when fraud has

been determined by FEMA. No premium

refund is allowed with this reason code. The

agent will retain the full commission, and

the company’s expense allowance will not

be reduced.

y Type of Refund: No refund allowed

y Years Eligible for Refund: N/A

y Cancellation Request: N/A

y Documentation: FEMA notification

24. Cancel/Rewrite Due to Map Revision,

LOMA, or LOMR. (TRRP reason 24)

Effective February 1, 2005, this reason

code is used to cancel and rewrite a

standard flood insurance policy to a PRP as

the result of a map revision, LOMA, or

LOMR. The standard policy will be canceled

and rewritten as a PRP as of inception. Use

New/Renewal Indicator ‘Z’ to report the new

policy. Premium from the canceled policy

will be applied to the PRP with the

difference refunded to the policyholder. No

30-day waiting period will apply to the PRP.

The agent will retain the full commission,

and the company’s expense allowance

will not be reduced. This rule applies to

the current policy year and

CN 7 October 1, 2005

one prior year provided that the effective

date of the map revision or LOMA/LOMR

occurred during the prior year.

y Type of Refund: Full

y Years Eligible for Refund: 2

y Cancellation Request: Must be received

during the policy year or within 6

months of the policy expiration date

y Documentation: Copy of revised map,

LOMA, or LOMR.

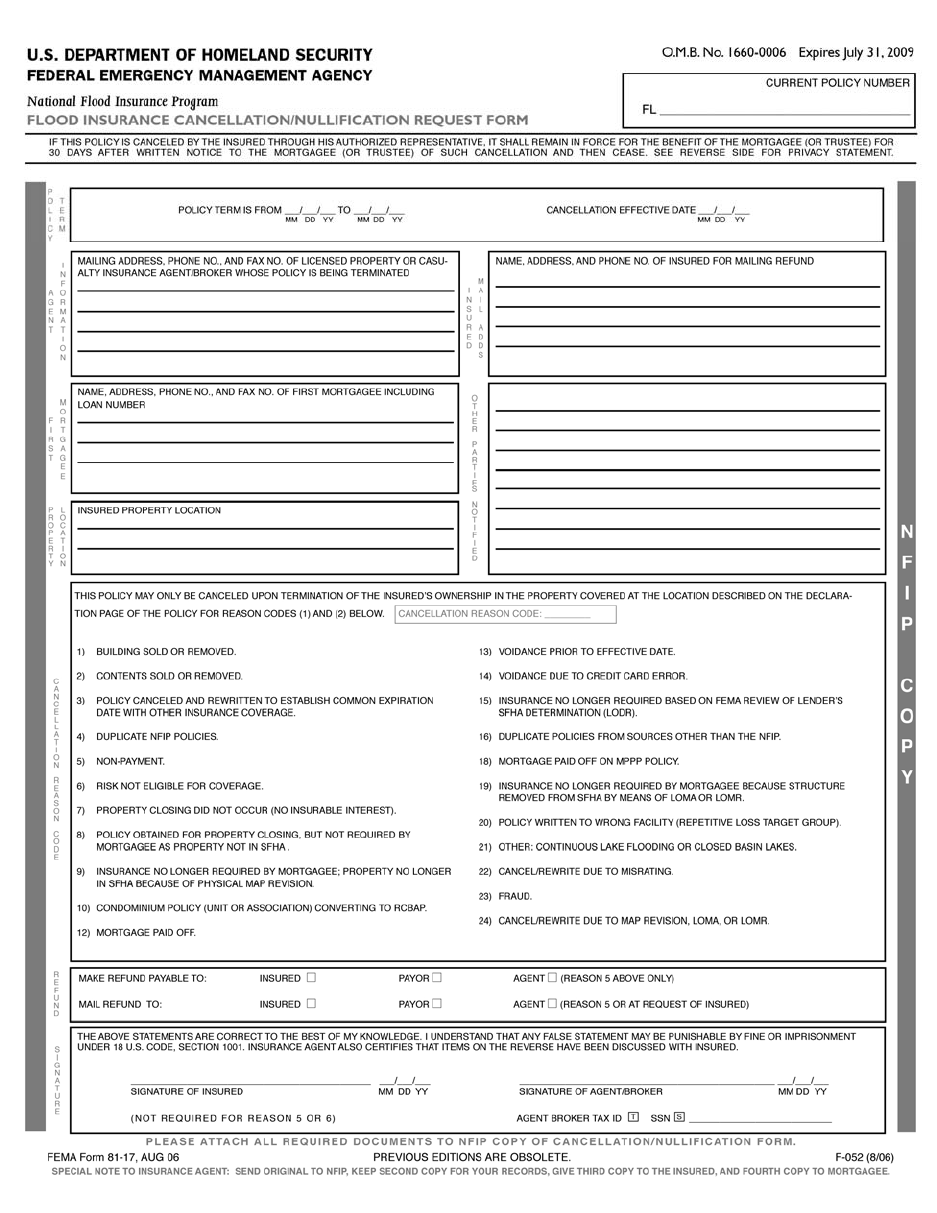

II. COMPLETING THE CANCELLATION/

NULLIFICATION REQUEST FORM

A. Current Policy Number

In the upper right corner of the form, enter the

NFIP policy number.

B. Policy Term

Enter the policy term and the cancellation

effective date.

C. Agent Information

Enter the complete name, mailing address,

phone number, and fax number of the producer.

D. Insured Mail Address

Enter the complete name, mailing address, and

phone number of the insured. If the insured has

moved to a new location, enter the new mailing

address.

E. First Mortgagee

Enter the complete name, mailing address,

phone number, and fax number of the first

mortgagee.

F. Other Parties Notified

Enter the complete name and mailing address of

all other interested parties who are to be notified,

such as any additional insured, the second

mortgagee, the loss payee, trustee, or disaster

assistance agency.

G. Property Location

Enter the location of the insured property.

H. Cancellation Reason Code

Check the reason for cancellation of the policy

and provide any additional information required.

I. Refund

Check the appropriate box to indicate to whom

the refund is to be made payable.

When a Cancellation/Nullification Request Form

is received that directs the NFIP to make a

premium refund to the PAYOR and the policy

has been endorsed showing the PAYOR as a

WYO Company or agency, the NFIP will make

the refund payable to the insured and mail the

refund in care of the producer. Check the

appropriate box to indicate to whom the refund

should be mailed.

J. Signature

The insured must sign and date the

Cancellation/Nullification Request Form for all

cancellation reason codes except 5 and 6. The

producer must sign, date, and enter a Tax I.D.

Number or Social Security Number in every

case. After completing the form, attach all

required supporting documents and mail the

original to the NFIP.

The producer should retain the second copy,

give the third copy to the insured, and the fourth

copy to the mortgagee.

After processing the Cancellation/Nullification

Request Form, the NFIP will send the producer,

mortgagee, and insured a notice of cancellation.

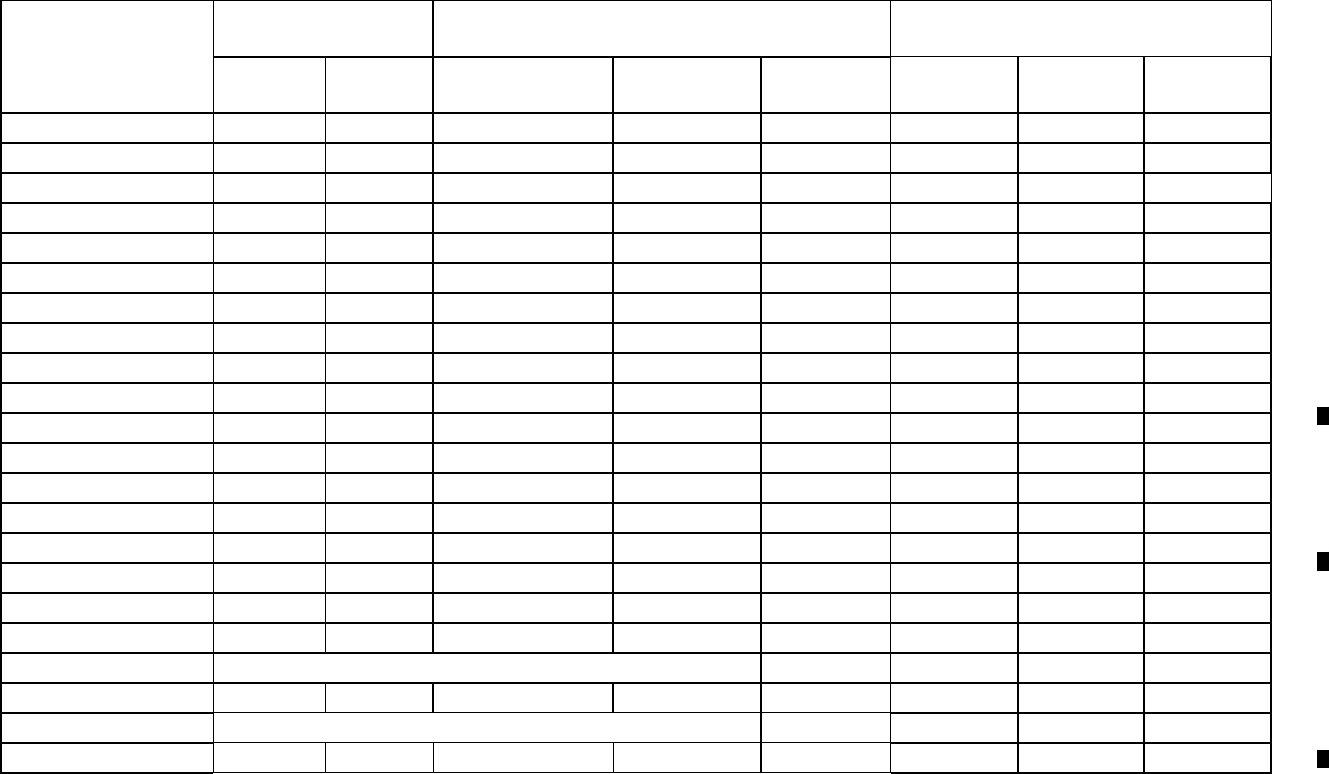

Processing Outcomes for Cancellation/Nullification

of a Flood Insurance Policy

PREMIUM REFUND

FEDERAL POLICY FEE

AND PROBATION SURCHARGE

PRODUCER COMMISSION

(Direct Business Only)

Reason Code for

Cancellation/

Nullification

(with TRRP Code)

Full Pro Rata Full Refund Pro Rata Fully

Earned

Full

Deduction

Pro Rata Retained

1

(

01

)

9 9

9

2

(

02

)

9 9

9

3

(

03

)

9 9

9

4

(

04

)

9 9

9

5

(

05

)

9 9

9

6

(

06

)

9 9

9

7

(

08

)

9 9

9

8

(

50

)

9 9

9

9

(

09

)

9 9

9

10

(

45

)

9 9

9

12

(

52

)

9 9

9

13

(

60

)

9 9

9

14

(

70

)

9 9

9

15

(

16

)

9 9

9

16

(

17

)

9 9

9

18

(

52

)

9 9

9

19

(

20

)

9 9

9

20

(

21

)

9 9

9

21

(

10

)

NO REFUND ALLOWED

9 9

22

(

22

)

9 9

9

23

(

23

)

NO REFUND ALLOWED

9 9

24

(

24

)

9 9

9

CN 8 October 1, 2005

CN 9 October 1, 2006

CN 10 October 1, 2006

NEXT SECTION

TABLE OF CONTENTS

PREVIOUS SECTION